Sigma-Pi Structure with Bernoulli Random Variables: Power-Law Bounds for Probability Distributions and Growth Models with Interdependent Entities

, , and

, , and {kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Abstract

:1. Introduction

2. Sigma-Pi Structure with Bernoulli Random Variables

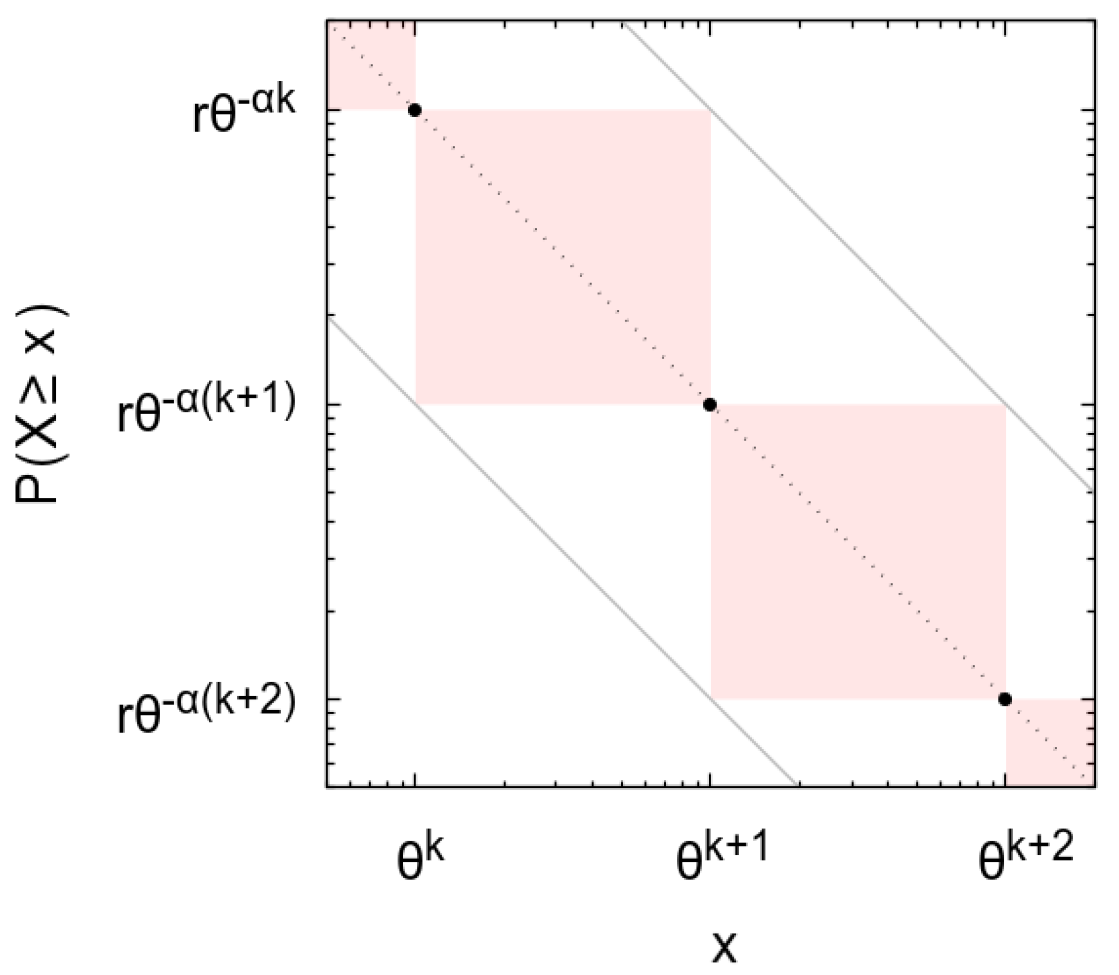

2.1. General Result

- (a)

- within-dependence: repeated variables within a single product term , i.e., . For example, in the variable appears twice (). In the extreme case in which all product terms have all variables distinct, we say that the Sigma-Pi structure has within-independence;

- (b)

- between-dependence: repeated variables in different product terms and , i.e., . For example, and share the variable (). In the extreme case in which any pair of product terms have all variables distinct, we say that the Sigma-Pi structure has between-independence.

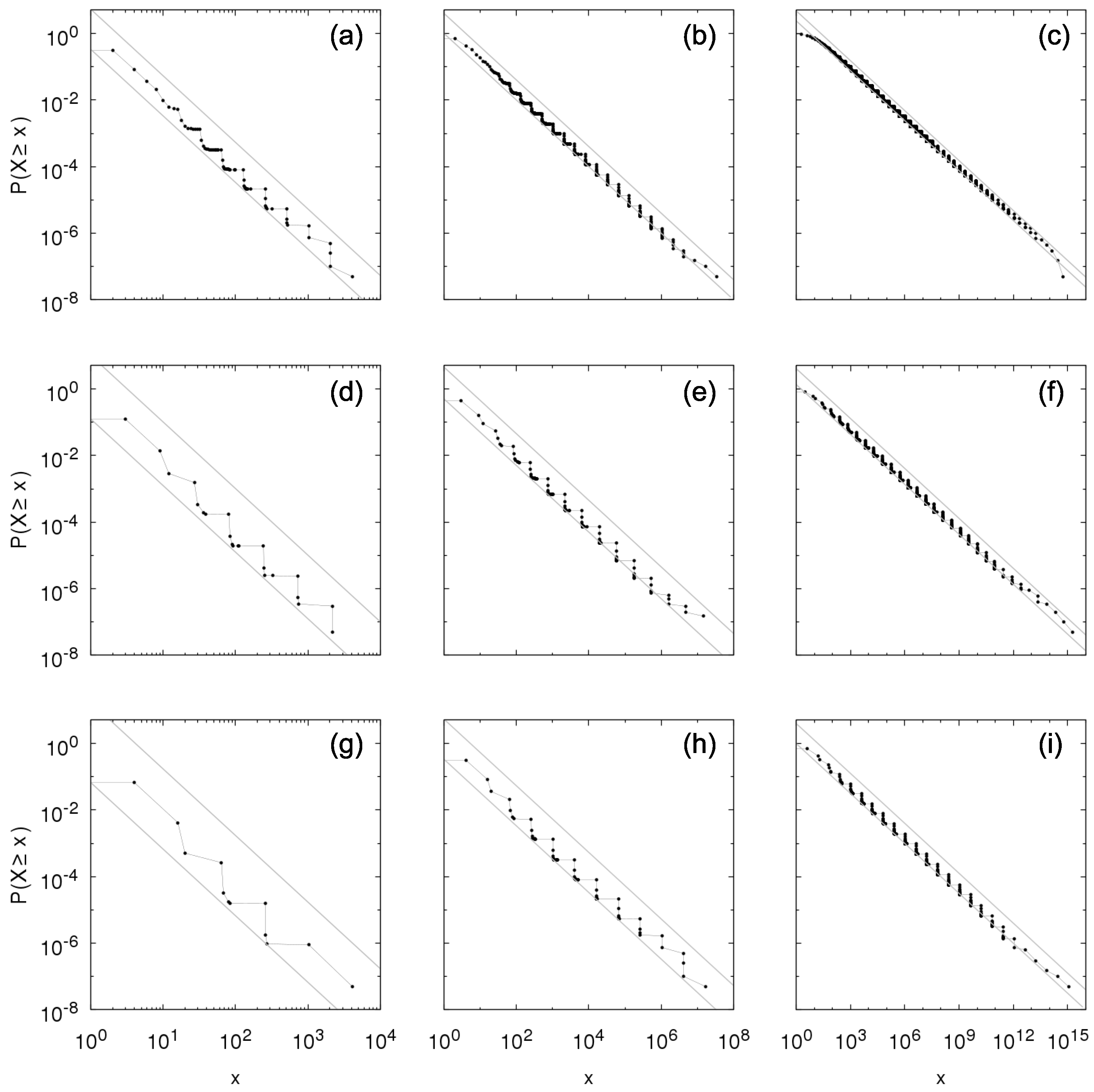

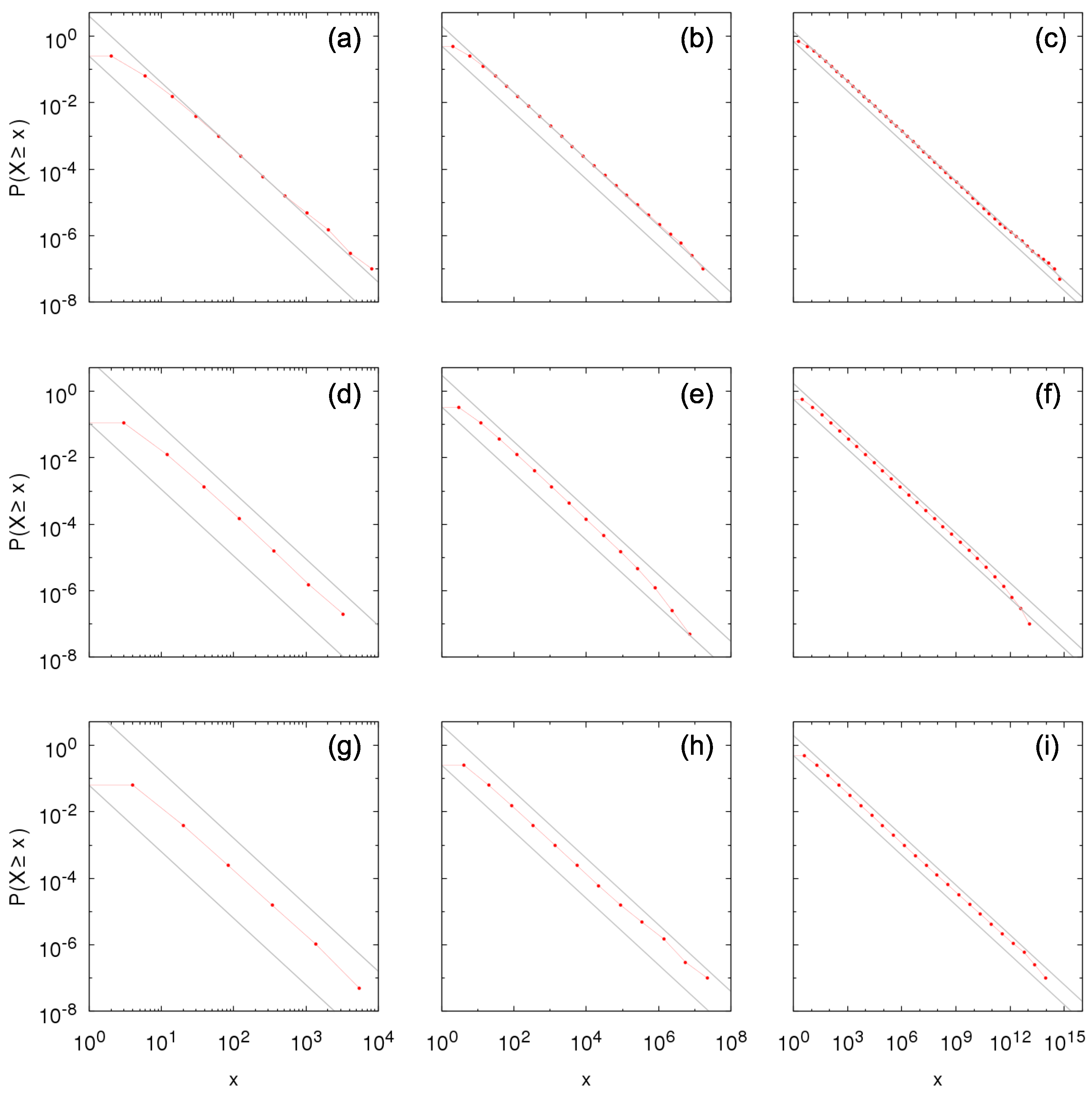

2.2. Within-Independence

- (i)

- between-independence: , ⇒, mutually independent.where the superscript indicates the nature of the between-dependence, the subscript indicates the nature of the within-dependence, and is the q-Pochhammer symbol [23]. For , using the expansion , we have

- (ii)

- Kesten between-dependence: , ⇒, .Note that for Kesten between-dependence there are restrictions on possible within-dependence: ; , , . For within-independence (, ), it reproduces the solution of the Kesten process.

2.3. Max-Pi Structure

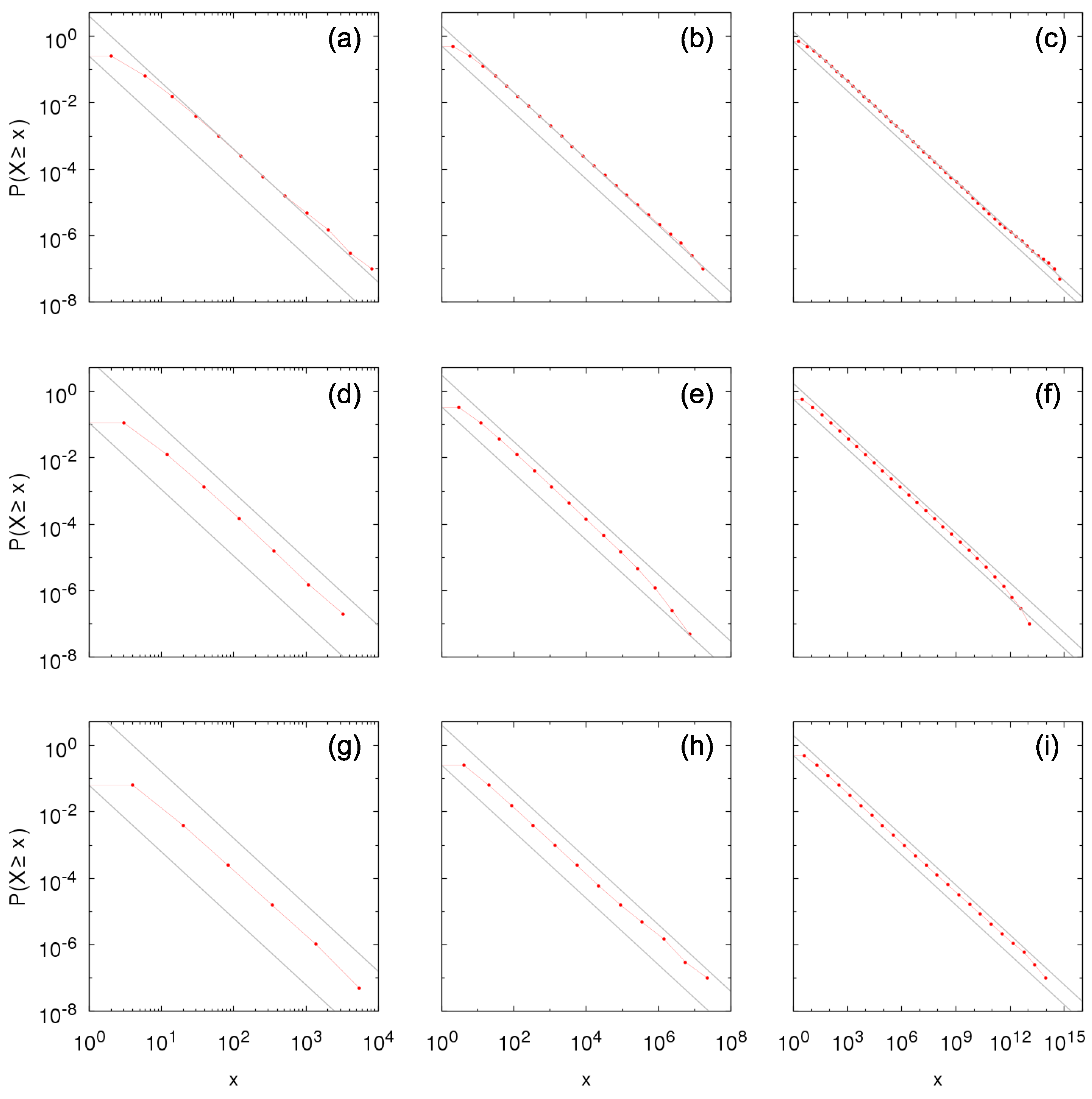

3. Growth Model with Bernoulli Random Variables

3.1. Growth-or-Death Model

3.2. Mixed between-Dependence

3.3. Within-Dependence as Temporal Dependence

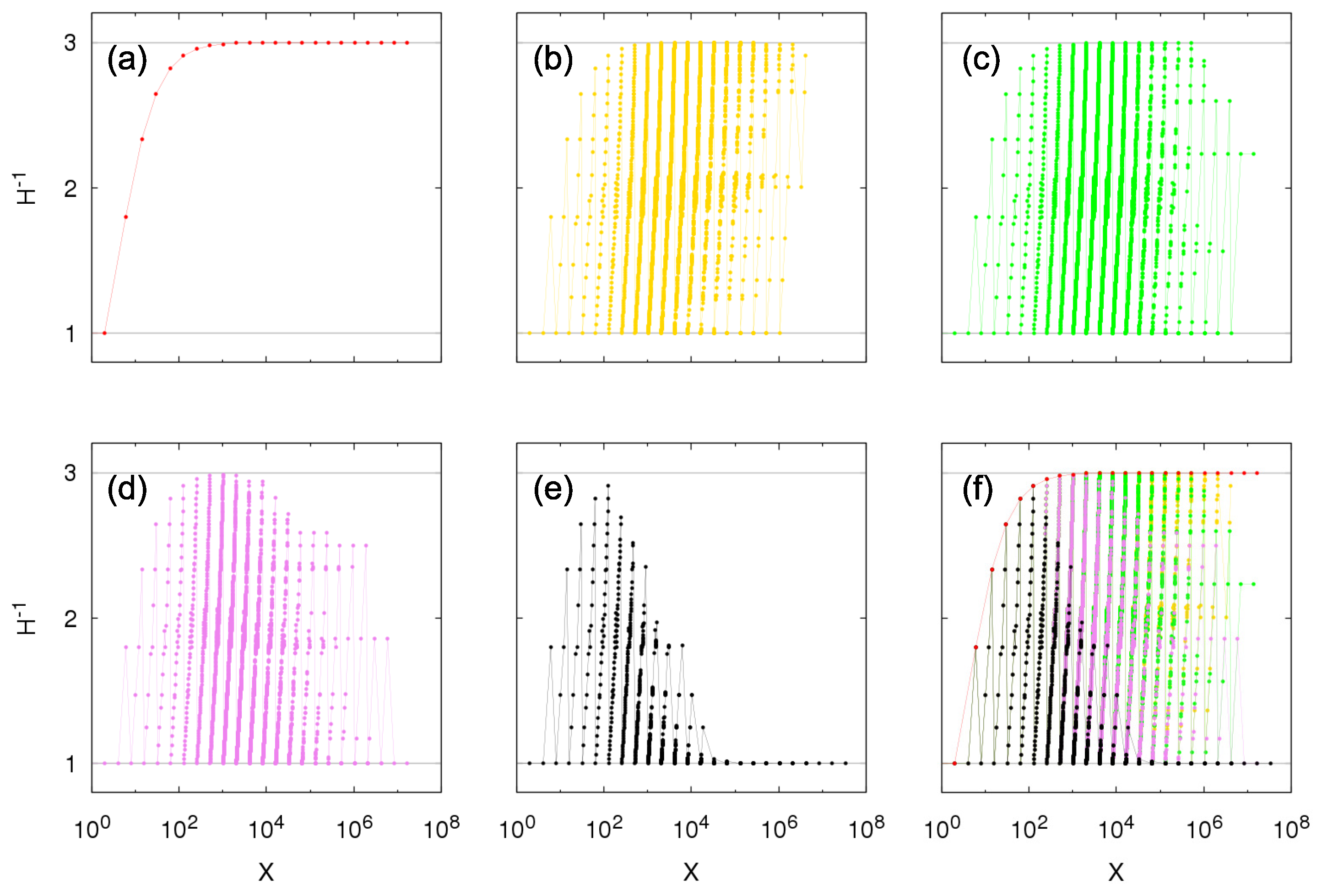

3.4. Contribution of Entities to the Total Sum

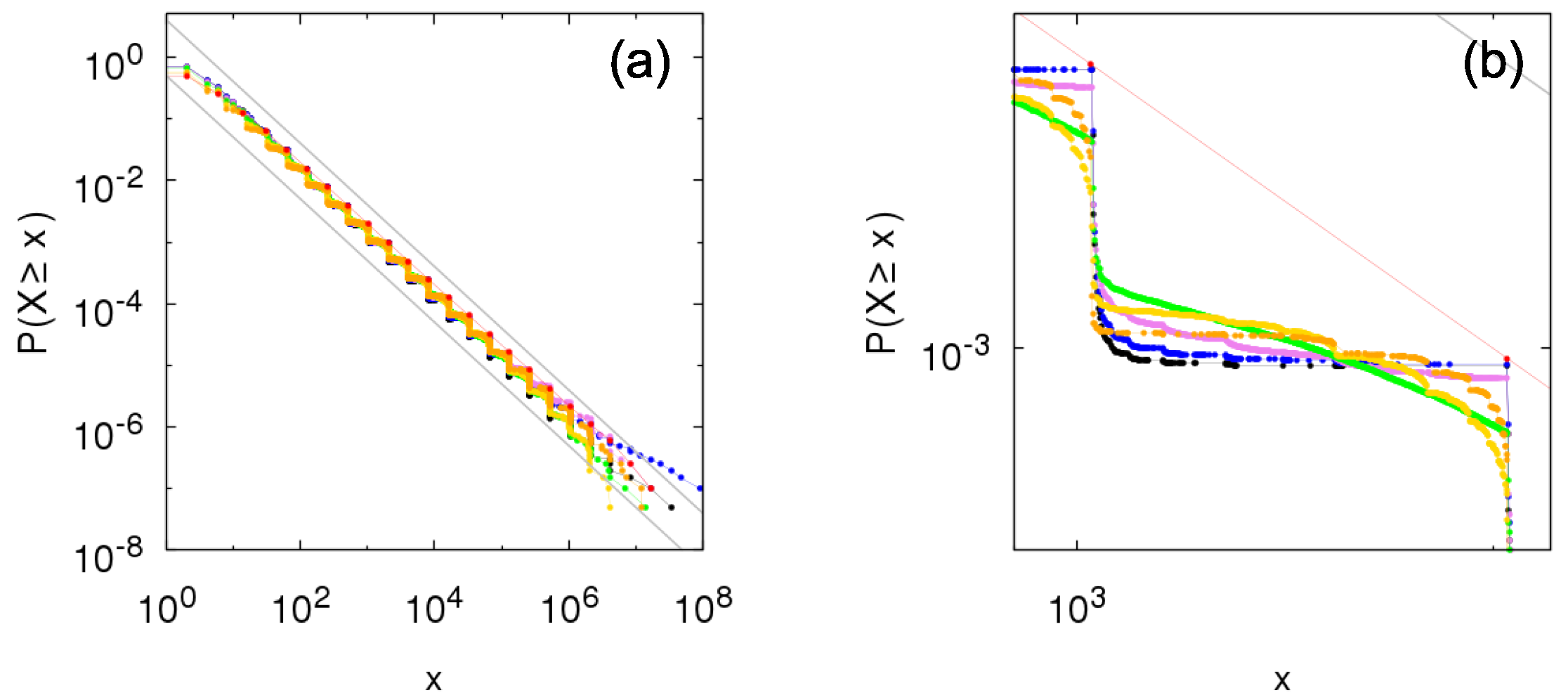

- (i)

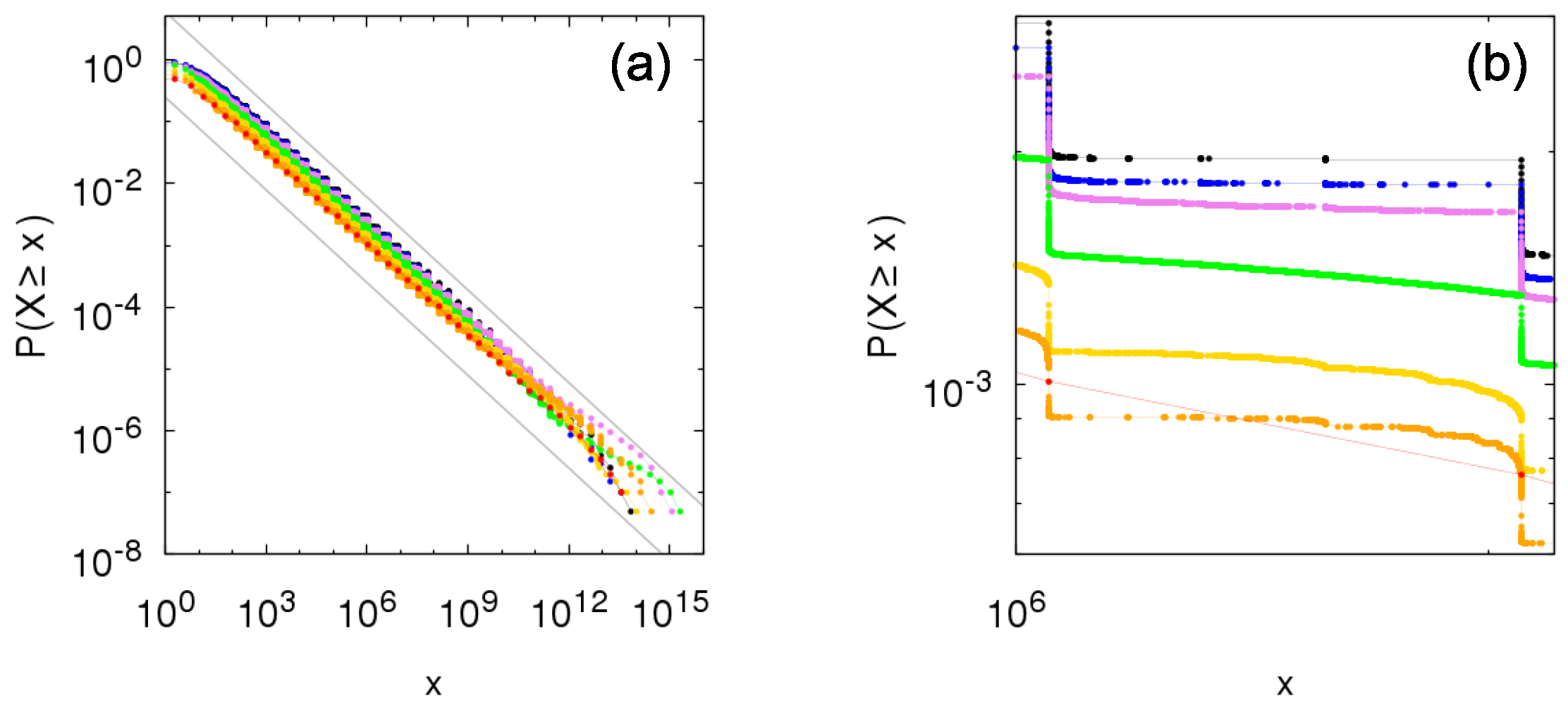

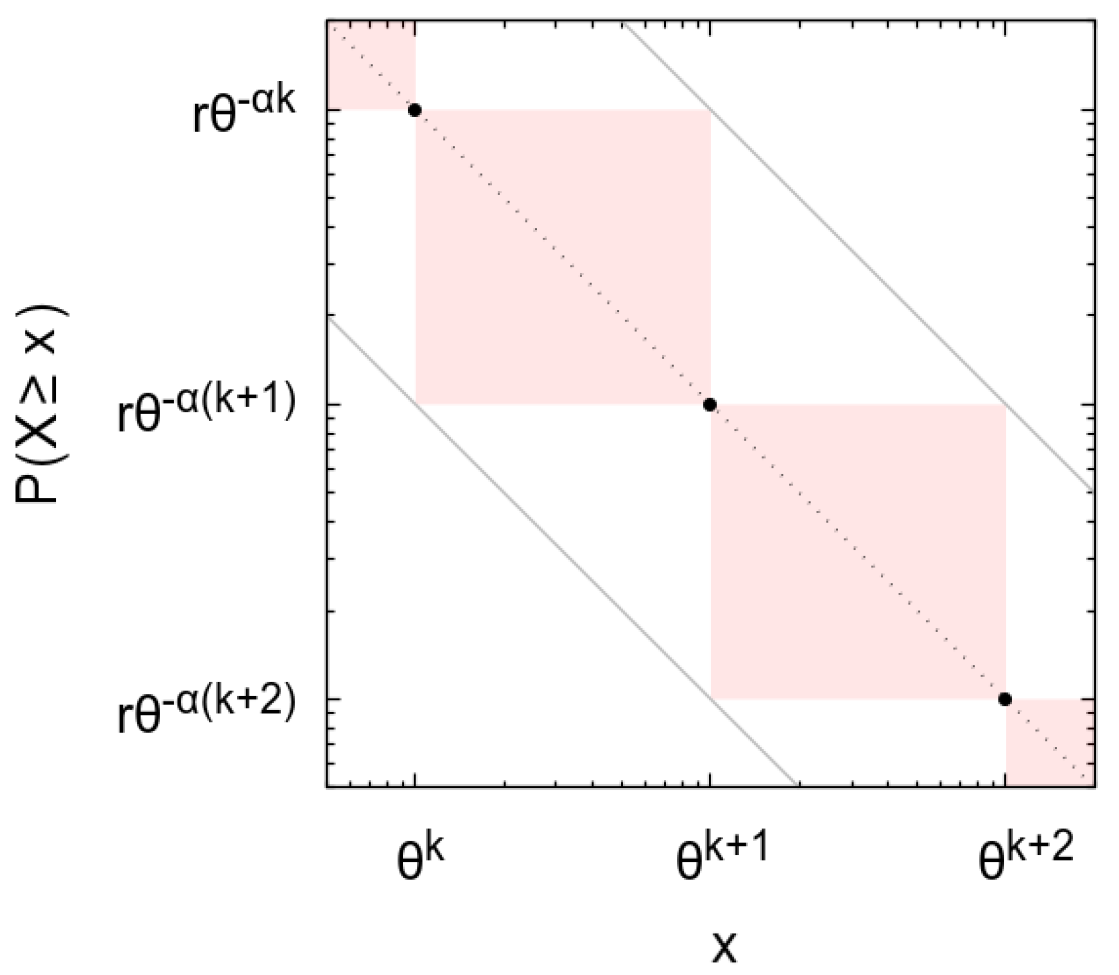

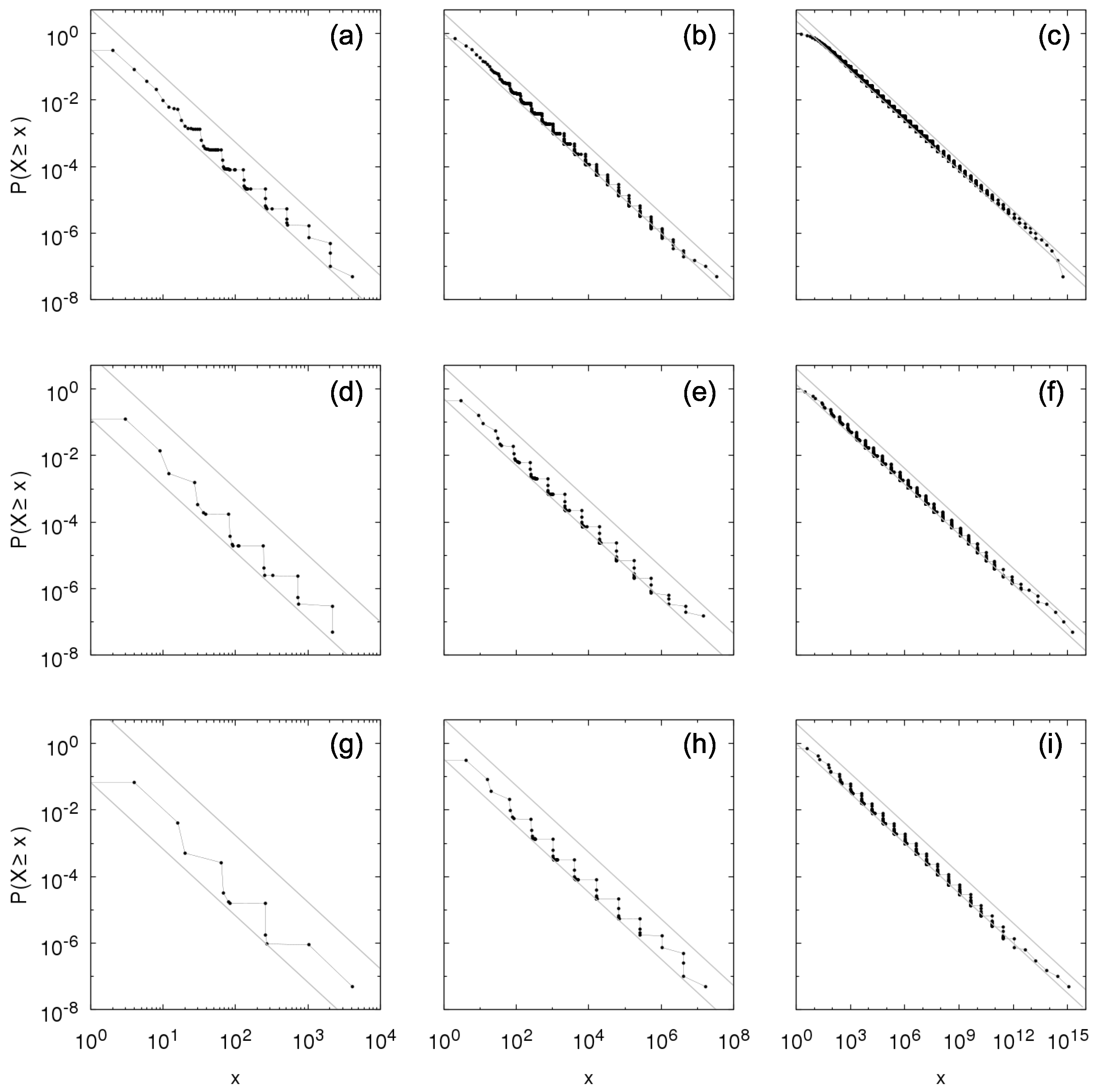

- between-independence: possible values of X are , , and the corresponding probabilities are computed by setting if is used to compose X and if otherwise (see Equation (4)):When this corresponds to a Poisson-binomial distribution [33,34], and it is the probability distribution of the number of existing entities at time t in this independence case.The particular values give . For large X, Herfindhal index (or ) has a small probability but larger than other values:so that, given the occurrence of a large X, the probability of is larger than the probability of .

- (ii)

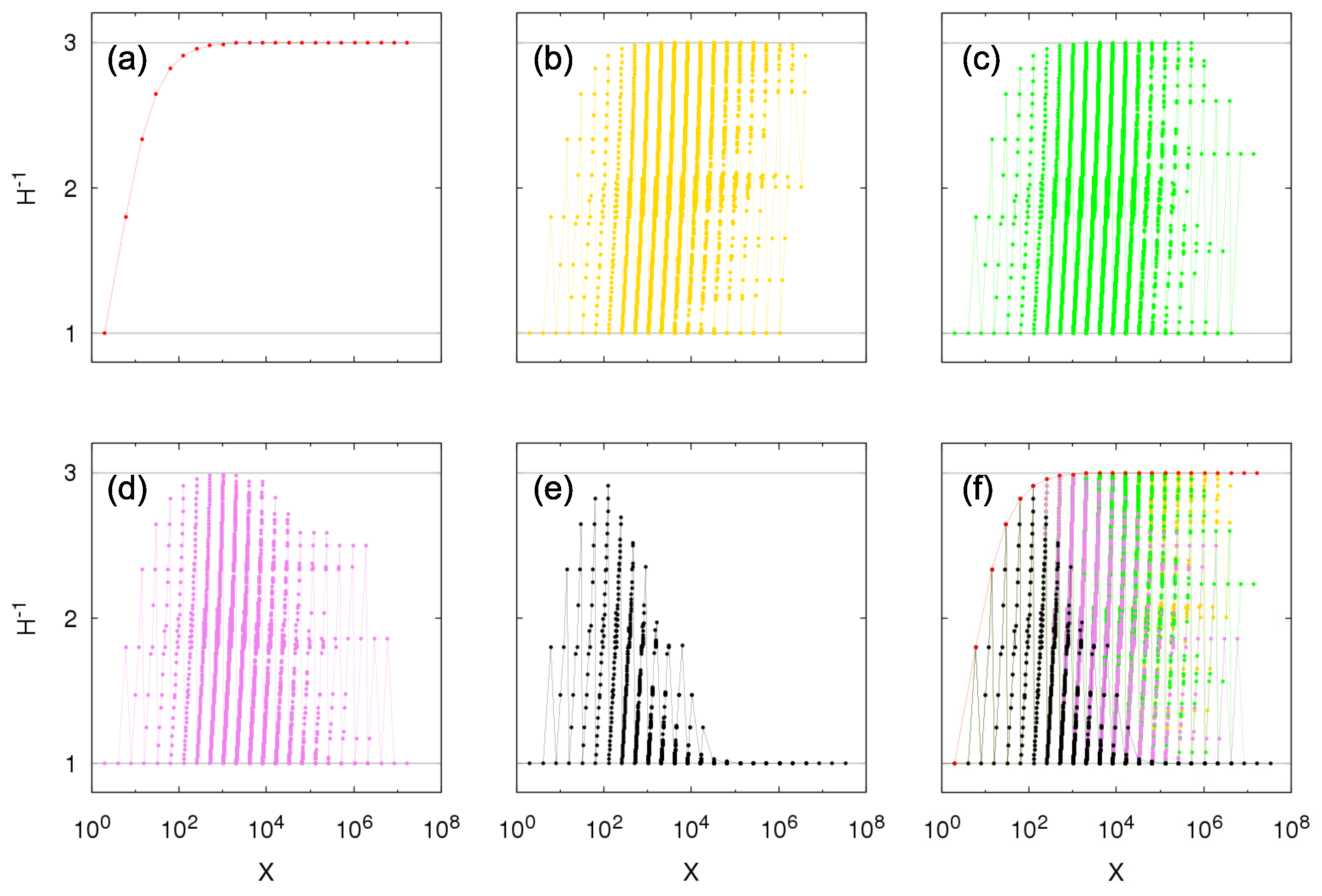

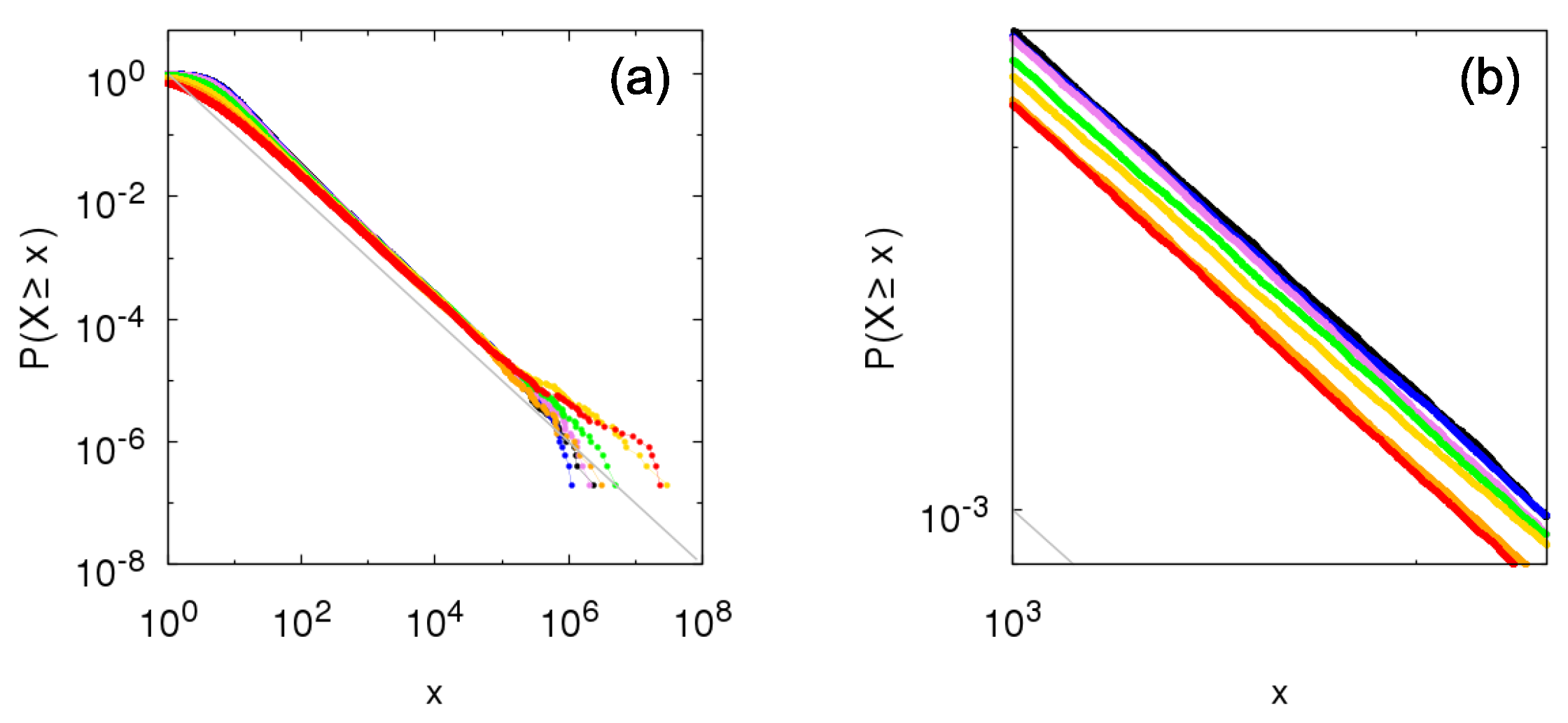

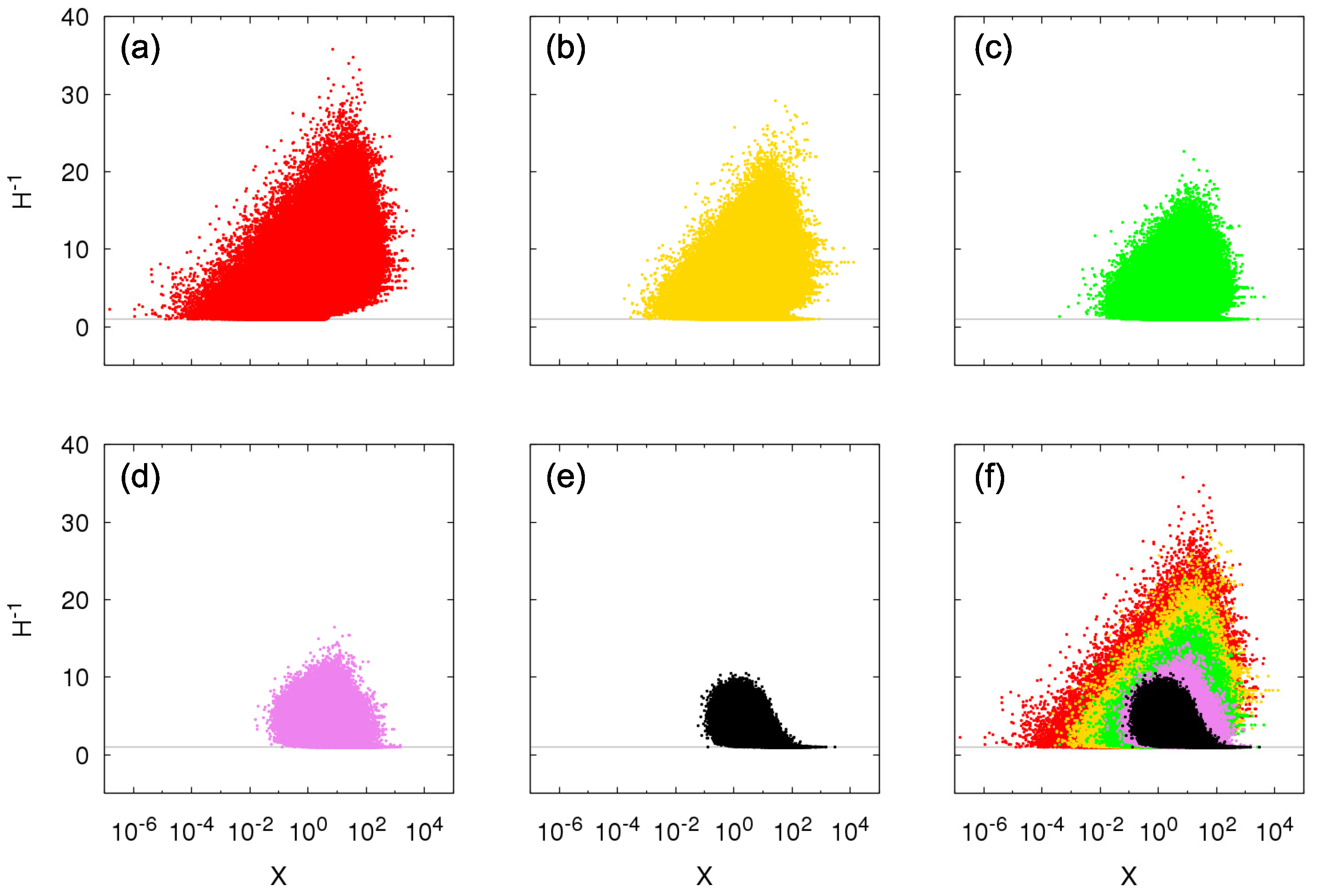

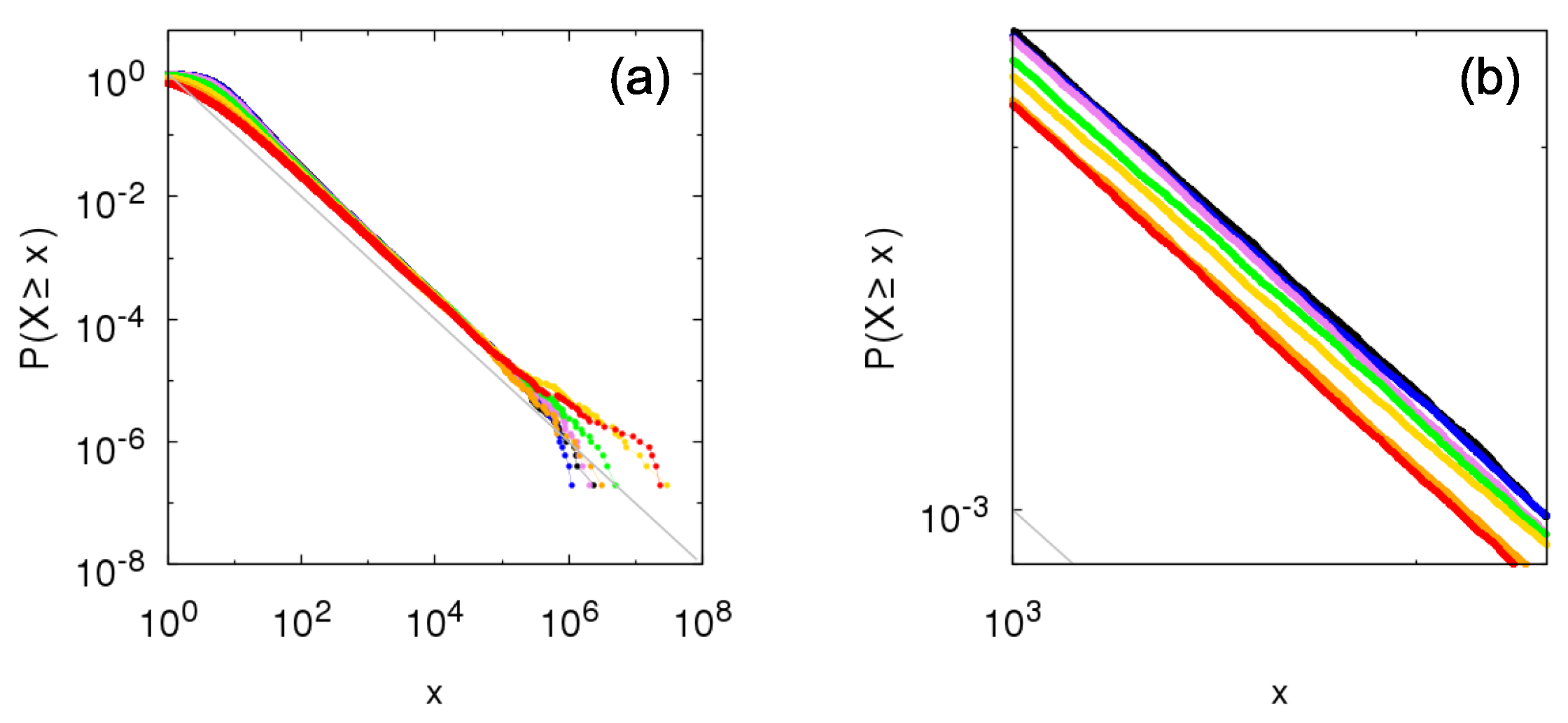

- Kesten between-dependence: possible values of X are and the corresponding probabilities areBecause of the restricted values of X in this Kesten case, the possible values of can be simply expressed as (see Equation (30))If , , as observed in Figure 6.

4. Growth Model with Half-Normal Random Variables

5. Final Remarks

Author Contributions

Funding

Institutional Review Board Statement

Informed Consent Statement

Data Availability Statement

Conflicts of Interest

Appendix A. Sigma-Pi with Bernoulli Random Variables (θ > 1)

References

- Sousa, A.M.Y.R.; Takayasu, H.; Sornette, D.; Takayasu, M. Power-law distributions from Sigma-Pi structure of sums of random multiplicative processes. Entropy 2017, 19, 417. [Google Scholar] [CrossRef] [Green Version]

- Buraczewski, D.; Damek, E.; Mikosch, T. Stochastic Models with Power-Law Tails; Springer: New York, NY, USA, 2016. [Google Scholar]

- Kesten, H. Random difference equations and renewal theory for products of random matrices. Acta Math. 1973, 131, 207–248. [Google Scholar] [CrossRef]

- Goldie, C.M. Implicit renewal theory and tails of solutions of random equations. Ann. Appl. Probab. 1991, 1, 126–166. [Google Scholar] [CrossRef]

- Anděl, J. Autoregressive series with random parameters. Statistics 1976, 7, 735–741. [Google Scholar] [CrossRef]

- Nicholls, D.F.; Quinn, B.G. The estimation of random coefficient autoregressive models I. J. Time Ser. Anal. 1980, 1, 37–46. [Google Scholar] [CrossRef]

- Klüppelberg, C.; Pergamenchtchikov, S. The tail of the stationary distribution of a random coefficient AR(q) model. Ann. Appl. Probab. 2004, 14, 971–1005. [Google Scholar] [CrossRef] [Green Version]

- Sousa, A.M.Y.R.; Takayasu, H.; Takayasu, M. Random coefficient autoregressive processes and the PUCK model with fluctuating potential. J. Stat. Mech. Theory Exp. 2019, 1, 013403. [Google Scholar] [CrossRef]

- Engle, R.F. Autoregressive conditional heteroscedasticity with estimates of the variance of United Kingdom inflation. Econometrica 1982, 50, 987–1007. [Google Scholar] [CrossRef]

- Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. J. Econ. 1986, 31, 307–327. [Google Scholar] [CrossRef] [Green Version]

- Engle, R.F. New frontiers for ARCH models. J. Appl. Econ. 2002, 17, 425–446. [Google Scholar] [CrossRef] [Green Version]

- Basrak, B.; Davis, R.A.; Mikosch, T. Regular variation of GARCH processes. Stoch. Process. Their Appl. 2002, 99, 95–115. [Google Scholar] [CrossRef] [Green Version]

- Takayasu, H.; Sato, A.H.; Takayasu, M. Stable infinite variance fluctuations in randomly amplified Langevin systems. Phys. Rev. Lett. 1997, 79, 966. [Google Scholar] [CrossRef]

- Sornette, D.; Cont, R. Convergent multiplicative processes repelled from zero: Power laws and truncated power laws. J. Phys. I 1997, 7, 431–444. [Google Scholar] [CrossRef]

- Sornette, D. Multiplicative processes and power laws. Phys. Rev. E 1998, 57, 4811. [Google Scholar] [CrossRef] [Green Version]

- Huynen, M.A.; Van Nimwegen, E. The frequency distribution of gene family sizes in complete genomes. Mol. Biol. Evol. 1998, 15, 583–589. [Google Scholar] [CrossRef] [PubMed]

- Amaral, L.A.N.; Buldyrev, S.V.; Havlin, S.; Salinger, M.A.; Stanley, H.E. Power law scaling for a system of interacting units with complex internal structure. Phys. Rev. Lett. 1998, 80, 1385. [Google Scholar] [CrossRef] [Green Version]

- Blank, A.; Solomon, S. Power laws in cities population, financial markets and internet sites (scaling in systems with a variable number of components). Phys. A 2000, 287, 279–288. [Google Scholar] [CrossRef]

- Picoli, S., Jr.; Mendes, R.S. Universal features in the growth dynamics of religious activities. Phys. Rev. E 2008, 77, 036105. [Google Scholar] [CrossRef] [PubMed]

- Takayasu, M.; Watanabe, H.; Takayasu, H. Generalised central limit theorems for growth rate distribution of complex systems. J. Stat. Phys. 2014, 155, 47–71. [Google Scholar] [CrossRef] [Green Version]

- Sutton, J. Gibrat’s legacy. J. Econ. Lit. 1997, 35, 40–59. [Google Scholar]

- Mikosch, T.; Rezapour, M.; Wintenberger, O. Heavy tails for an alternative stochastic perpetuity model. Stoch. Process. Their Appl. 2019, 129, 4638–4662. [Google Scholar] [CrossRef] [Green Version]

- Weisstein, E.W. q-Pochhammer Symbol. MathWorld–A Wolfram Web Resource. 2019. Available online: http://mathworld.wolfram.com/q-PochhammerSymbol.html (accessed on 12 February 2019).

- Grincevićius, A.K. One limit distribution for a random walk on the line. Lith. Math. J. 1975, 15, 580–589. [Google Scholar] [CrossRef]

- Wergen, G. Records in stochastic processes—Theory and applications. J. Phys. A 2013, 46, 223001. [Google Scholar] [CrossRef]

- Saichev, A.I.; Malevergne, Y.; Sornette, D. Theory of Zipf’s Law and Beyond; Springer-Verlag Berlin Heidelberg: Berlin, Germany, 2009. [Google Scholar]

- Hisano, R.; Sornette, D.; Mizuno, T. Predicted and verified deviations from Zipf’s law in ecology of competing products. Phys. Rev. E 2011, 84, 026117. [Google Scholar] [CrossRef] [PubMed] [Green Version]

- Malevergne, Y.; Saichev, A.; Sornette, D. Zipf’s law and maximum sustainable growth. J. Econ. Dyn. Control 2013, 37, 1195–1212. [Google Scholar] [CrossRef] [Green Version]

- Sato, A.H.; Takayasu, H.; Sawada, Y. Invariant power law distribution of Langevin systems with colored multiplicative noise. Phys. Rev. E 2000, 61, 1081. [Google Scholar] [CrossRef] [PubMed]

- Morita, S. Power law in random multiplicative processes with spatio-temporal correlated multipliers. EPL 2016, 113, 40007. [Google Scholar] [CrossRef] [Green Version]

- Investopedia. Herfindahl-Hirschman Index—HHI. 2019. Available online: http://investopedia.com/terms/h/hhi.asp (accessed on 12 February 2019).

- Thouless, D.J. Electrons in disordered systems and the theory of localization. Phys. Rep. 1974, 13, 93–142. [Google Scholar] [CrossRef]

- Wang, Y.H. On the number of successes in independent trials. Stat. Sin. 1993, 3, 295–312. [Google Scholar]

- Hong, Y. On computing the distribution function for the Poisson binomial distribution. Comput. Stat. Data Anal. 2013, 59, 41–51. [Google Scholar] [CrossRef]

- Weisstein, E.W. Half-Normal Distribution. 2019. Available online: http://mathworld.wolfram.com/Half-NormalDistribution.html (accessed on 12 February 2019).

Publisher’s Note: MDPI stays neutral with regard to jurisdictional claims in published maps and institutional affiliations. |

© 2021 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Share and Cite

Yamashita Rios de Sousa, A.M.; Takayasu, H.; Sornette, D.; Takayasu, M. Sigma-Pi Structure with Bernoulli Random Variables: Power-Law Bounds for Probability Distributions and Growth Models with Interdependent Entities. Entropy 2021, 23, 241. https://doi.org/10.3390/e23020241

Yamashita Rios de Sousa AM, Takayasu H, Sornette D, Takayasu M. Sigma-Pi Structure with Bernoulli Random Variables: Power-Law Bounds for Probability Distributions and Growth Models with Interdependent Entities. Entropy. 2021; 23(2):241. https://doi.org/10.3390/e23020241

Chicago/Turabian StyleYamashita Rios de Sousa, Arthur Matsuo, Hideki Takayasu, Didier Sornette, and Misako Takayasu. 2021. "Sigma-Pi Structure with Bernoulli Random Variables: Power-Law Bounds for Probability Distributions and Growth Models with Interdependent Entities" Entropy 23, no. 2: 241. https://doi.org/10.3390/e23020241